ABOUT THE VALUABLE HOUSE TAX

25 December 2019

The Law on the Amendment of Digital Service Tax numbered 7194 and some laws and Decree Law numbered 375 (the “Law”) was published in the Official Gazette on 7 December 2019.

The aforementioned Law brought new provisions to the Real Estate Tax Law (“RETL”) and introduced the valuable house tax into our tax system. The provisions relating to this tax came into force on the day of its publication.

1. Valuable House Tax in General

With the new legislation, it is regulated that the residential immovable properties located within the borders of Turkey, whose value is TRY 5,000,000 or more, will be subject to the valuable house tax. The taxpayers of the tax are the owners of the immovable property in question, the holder of the usufruct right if any, or in case neither exists, the adverse possessors.

The owners are liable in proportion with their shares in case of shared ownership, and jointly in case of joint ownership. Both in shared ownership and in joint ownership the total value of the immovable property will be taken into consideration in calculation.

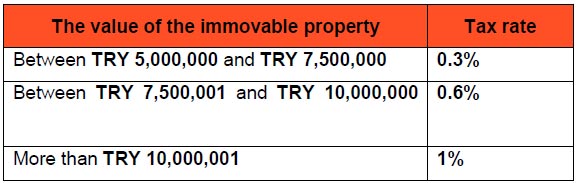

2. Tax Rates:

Tax rates according to the value of residential immovable properties are as follows:

3. Valuation

The immovable properties whose value are determined to be TRY 5,000,000 or more as a result of the valuation made or have been made by the General Directorate of Land Registry and Cadastre (“GDLRC”) are announced on the website of GDLRC in a manner that the persons concerned can reach and the persons concerned are also notified officially.

4. Objection to the Valuation

The taxpayer, who has been served with the aforementioned notification, must object to the valuation in writing within 15 days either in person or through an authorized representative, and if it is not objected within this period, the price determined as a result of the valuation is finalized.

The objection can be made to GDLRC or any land registry office to be conveyed to GDLRC. The objections made during the period shall be evaluated and concluded within 15 days, and this finalized value shall be notified in the same manner by announcement and notification to the persons concerned.

5. Judicial Remedies following the Objection

An administrative lawsuit can be filed in Administrative Courts within 30 days as of the notification as a result of the objection. In addition, taxpayers can file a lawsuit in Tax Courts within 30 days of being notified of the tax liability.

During this process, declarations and payments should be made with reservation. Otherwise, the reimbursement of the tax payments cannot be requested after the trial.

6. Declaration and Payment of the Tax

The taxpayer shall declare the tax value of the residential immovable property in question and the value determined by GDLRC to the authorised tax office of the Revenue Administration where the immovable property is located until the end of the 20th day of February of the year following the year the value of the immovable property exceeded TRY 5,000,000.

Tax is declared by the taxpayer in the following years as well and levied and accrued annually by the tax office.

Whilst taxpayers in shared ownership shall provide individual declarations taxpayers with joint ownership may provide declarations jointly or individually.

Tax shall be paid until the end of February and August of the relevant year in two equal instalments.

7. Exemptions

The law exempted the following immovable properties from the valuable house tax, even when the immovable property is residential:

- Immovable properties of which general and special budgeted administrations, municipalities and universities have ownership or usufruct rights;

- The immovable properties owned by the persons who have only one residential immovable property within the borders of Turkey (except those who have a legal guardian obliged to look after them and who are not over the age of 18) who certify that they have no income or whose income consists exclusively of the monthly pension they receive from the social security institutions;

- Some of the immovable properties within diplomatic mission,

- The newly built immovable properties which are registered in the name of those whose main activity subject is building construction and have not yet been put up for sale, transfer and assignment.

Should you have any queries on the above, please do not hesitate to contact us.